When you are exploring the notion of a non-traditional home loan, you’ve got heard of desire-only mortgage loans

Get A quote

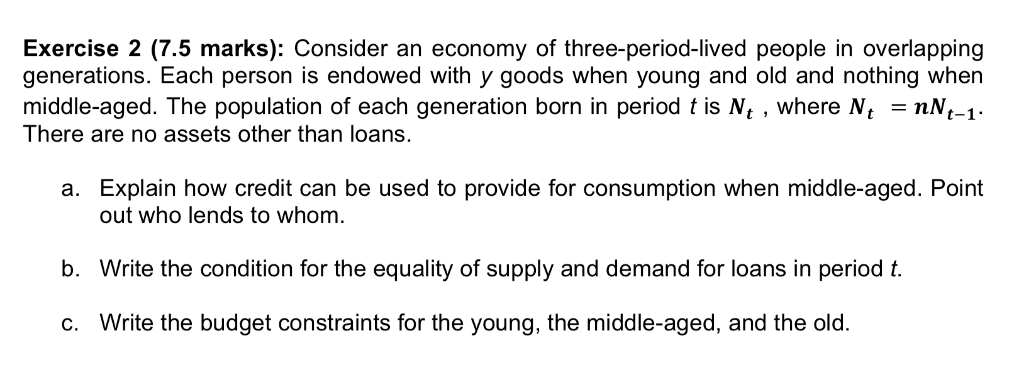

Such funds have its advantages and disadvantages, but according to your unique situation and borrowing from the bank requires, it could be the ideal mortgage for you.

What exactly is a destination-simply mortgage?

A consistent mortgage repayment includes both attention and you may prominent, but with an appeal-simply mortgage, consumers have the opportunity to only pay notice to own a portion of one’s home loan title. Interest-just repayments have a tendency to generally last for the first several years; well-known examples of financing terminology are five years, eight years, otherwise 10 years. Due to the fact borrowers are just repaying interest throughout the people first couple of ages, their costs are all the way down, but there is however an effective caveat: to meet up with the main repayments, costs was highest following the focus-merely period is up, if you do not re-finance. At exactly the same time, you won’t initiate strengthening family collateral unless you initiate purchasing on their principal.

How does an appeal-simply financial works?

The initial chronilogical age of an attraction-merely financial shall be appealing for some consumers, but it’s important to look at the entire picture when deciding whether or not this type of mortgage is best suited for your.

To higher know the way an interest-just home loan really works, let’s consider the second analogy: an interest-only 29-seasons mortgage having $150,000 which have an initial five-seasons desire-simply title. In the event the interest are step 3.5 per cent, this new monthly premiums could be $ (leaving out other costs, like assets taxation or potential HOA costs). Due to the fact attract-merely months is over, although not, payments beginning to increase since the principal begins amortizing, and you’re up coming spending both prominent and you can appeal more than a shorter time period. Within this particular example, the new $ part of your payment jumps up to $750 while it began with the fresh new sixth year. It is because you’re using both prominent and you may desire amortized over a twenty five-season months in the place of a 30-year several months.

Variety of focus-simply mortgage loans

As well as different conditions towards the focus-simply period, there are also different types of focus-just loans altogether. Examining the different types of appeal-simply mortgages a lot more in the-depth makes it possible to determine what type of appeal-simply mortgage works well with you.

Adjustable-speed attract-simply mortgages.

Regardless of if our very own example more than is actually having a predetermined-speed circumstance, interest-only mortgage loans typically have adjustable prices. Interest-just mortgages are prepared while the step 3/1, 5/1, 7/step 1, otherwise ten/step 1 finance. The initial number represents the eye-simply percentage several months, and also the next amount means what number of moments the brand new costs is modified. If you were to take-out a beneficial 7/step 1 interest-merely mortgage, by way of example, you’d enjoys interest-simply payments to own seven age along with your interest rate would be modified a single time on the longevity of the loan. In the event the rate try adjusted, it does echo economy costs, which means that your price you are going to sometimes rise or off. But it does have the potential to boost, there are rate caps one maximum how high they’re able to go and borrowers will know what the speed limit are in the future of time.

Fixed-speed focus-merely mortgages.

Although repaired-price notice-simply mortgages commonly nearly given that common as the changeable-speed notice-only mortgage loans, they do exist and certainly will become an appealing solution when mortgage cost are at an all-time reasonable. Possession create typically promote interest rates which can be quite lower than mediocre for the basic several months however they are next a small high through to amortization.

Jumbo mortgage loans.

If you are searching in order to use beyond traditional mortgage limits and also you are also exploring the concept of an interest-just mortgage, you could take advantage of a destination-only jumbo home loan, which can be loans that allow borrowing limits up to $650,000. This could be a good option having buyers who will be hesitant https://paydayloanalabama.com/remlap/ to spend with the principal because they has actually concerns about treating that money after they offer their home.

Interest-simply HELOCs.

House security credit lines, otherwise HELOCs, functions instance playing cards. He is theoretically second mortgage loans that provide property owners the ability to borrow funds when using their houses as the security. If you are thinking about taking out a beneficial HELOC, you could have the option to take out an interest-merely HELOC. Similar to focus-simply mortgages, obtain pay only straight back appeal first. If the borrower provides a thirty-year cost several months, the interest-just months might only function as the basic ten years, when the newest borrower gets the choice to fool around with as often of one’s credit line as needed. Toward left 20 years, the financing range try frozen therefore the equilibrium are paid back.

Rates research

Consumers is also generally speaking anticipate paying at the least a great 0.25 % advanced when taking aside an attraction-simply financing, otherwise an interest rate that is as much as 0.125 so you can 0.375 per cent greater than the speed to own an amortizing mortgage. Prior to a last choice on the which type of financial to take-out, it can be useful to manage a cost testing.

What if you take away a great $2 hundred,000 attract-just mortgage that have a totally amortizing Arm or repaired price. Is what you could anticipate paying every month predicated on hypothetical interest rates, without providing assets fees, HOA, insurance rates, and other can cost you under consideration.

From the these pricing, for the short term, an interest-just Sleeve will cost you $ faster every month for each and every $100,000 lent from inside the seven-12 months desire-just period compared to a thirty-season repaired-price mortgage, and you may $ shorter 30 days compared with a completely amortizing 7/step one Case. Forecasting the whole rates along side life of the borrowed funds can also be be difficult because when you are looking at adjustable rates, the thing you will know from the ahead of time ‘s the speed limit. With this specific advice, but not, you could calculate minimal and you may restriction existence costs.

Summary with the attention-merely mortgages

An appeal-merely mortgage are going to be an effective way having consumers to save money on its mortgage, but to completely take advantage of the rates-saving experts these particular type of money promote, it means refinancing in order to a vintage home loan ahead of the interest-only identity stop. As an alternative, specific borrowers will sell their property up until the desire-only term ends, which can make attention-just mortgages the ideal selection for borrowers who don’t thinking about being in their house toward long haul.

Conventional changeable-speed mortgages that can tend to be dominant as part of the month-to-month payments is another option to look at if you’re looking to possess all the way down-than-average interest levels at the beginning of your loan, however, you would including need to pay to your prominent from the delivery, too.

Regardless if you are looking to take out an appeal-merely financial, re-finance a recently available attract-only mortgage, otherwise explore your almost every other financial options (eg a supply), Filo Mortgage has arrived to simply help. E mail us today to discover more in order to explore the other choice.